If you followed the seasonal investing advice of “sell in May and go away,” you may want to reconsider because the outlook for the economy and financial markets will likely be determined in the coming months.

Several major events, datasets, progress reports, and deals are due this summer. By fall, the impact of President Donald Trump’s tariffs and fiscal policies should be clearer, giving the Federal Reserve enough confidence to act on interest rates.

Here’s a look at the factors that will tip the scales:

One Big Beautiful Bill

A key piece could come as soon as this week. Trump has set a July 4 deadline for Congress to pass his so-called One Big Beautiful Bill, which contains his tax cuts and spending priorities.

While the House of Representatives passed one version of the legislation and the Senate advanced a separate one, the GOP’s narrow majorities in both chambers make the timing of the eventual package and its exact provisions less certain.

All the congressional logrolling that’s needed could push the timeline past July 4, especially now that a few Republicans have announced they will not seek re-election, making them less susceptible to Trump’s arm-twisting.

Wall Street expects the tax cuts to juice the economy and the stock market, while the bond market will watch the bill’s impact on U.S. debt. The Congressional Budget Office has estimated the Senate’s version of the bill will add nearly $3.3 trillion to deficits over a decade.

More fiscal sticker shock could send Treasury yields higher and add more pressure on the dollar, which is already down 10% this year, its worst first-half performance in more than 50 years.

Debt ceiling

Treasury Secretary Scott Bessent has estimated that the U.S. will no longer be able to pay its bills by mid to late summer, unless the debt ceiling is raised.

While he has vowed that the U.S. will never default, it’s up to Congress to raise the debt limit so that the Treasury Department can issue fresh bonds to service interest expenses and maturities.

The One Big Beautiful Bill would increase the debt ceiling by trillions of dollars. In the meantime, the Treasury Department has been using its extraordinary cash management measures to avoid default.

Bessent said last week he extended his department’s authority to use those extraordinary measures to July 24, in an apparent reminder for Congress to raise the debt ceiling before its typical August recess.

Failure to raise the debt limit and prevent a U.S. default would spark a global financial meltdown.

Tariffs and trade deals

Trump administration officials have been saying since “Liberation Day” in April that major trade deals are imminent. So far, the U.S. has reached agreements with the U.K. and China, while negotiations with other top trade partners continue.

Meanwhile, the 90-day pause on Trump’s “reciprocal” tariffs will expire on July 9, after which they would spike back to levels that triggered an epic stock market selloff.

Bessent has signaled flexibility on that deadline, saying a dozen or so trade deals could be reached by Labor Day. But over the weekend, Trump reiterated his desire to dispense with any further talks and unilaterally set a tariff rate on each country.

A sudden return to high tariffs would deliver another jolt to Wall Street, which had been expecting duties to eventually settle at 10% for most countries and 30% for China—manageable levels that could largely be absorbed without too much pain.

Federal Reserve

Tariffs and their impact on inflation will heavily influence the central bank as it weighs whether to trim interest rates. Pricing data so far hasn’t revealed a big impact from tariffs, and a few Fed officials have said that’s evidence that inflation is tame enough to justify rate cuts.

But Fed Chairman Jerome Powell and other policymakers have indicated they need at least a few more months of data to be confident that inflation is indeed on the right track.

If the upcoming data show that any tariff-related inflation effects are only one-offs that aren’t raising consumers’ inflation expectations over the longer run, then rate cuts could come in the fall.

While Trump has demanded the Fed lower rates immediately, he could also make it harder for policymakers to do that. They may more reluctant to cut just to prove to markets that they are independent from political pressure. Re-escalation of tariffs could muddy the inflation picture. The naming of a “shadow” Fed chair could even stir a revolt on the Federal Open Market Committee.

Corporate Earnings

Starting in July, earnings reports for the second quarter will start coming out, giving Wall Street a more fulsome view of how tariffs—and the economic uncertainty they’ve caused—are affecting profits as well as the outlook for profits.

Because companies rushed to stock up on imports earlier in the year to get ahead of tariffs, first-quarter results didn’t fully reflect higher rates.

But those stockpiles are being exhausted, forcing companies to hike prices on consumers or eat tariff costs and shrink profit margins.

Also factoring into earnings will be how much or how little companies plan to invest and hire in an economy that is slowing amid Trump’s trade war.

The White House’s fiscal policies will sway earnings too, as tax cuts, the end of certain tax credits, more spending on defense, and less spending on the social safety net ripple through Corporate America and consumers.

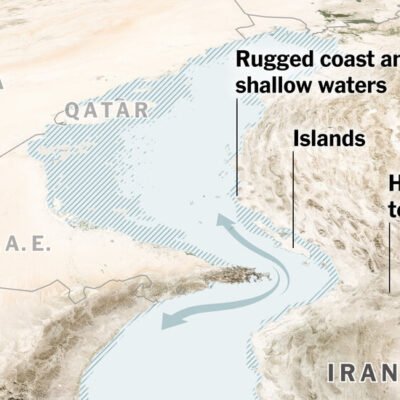

Wildcard: The Middle East

A tenuous ceasefire has taken hold between Israel, Iran and the U.S., sending oil prices lower as markets worry less about a sudden supply disruption.

But Trump has said he is open to bombing Iran again if it’s necessary to cripple Tehran’s nuclear program. That’s as conflicting reports emerge over how much Iran’s capabilities have actually been damaged.

Renewed fighting could set off another surge in crude prices, sapping consumers of spending power, reigniting inflation, and further complicating the outlook for Fed rate cuts and the economy.

Have a great summer.